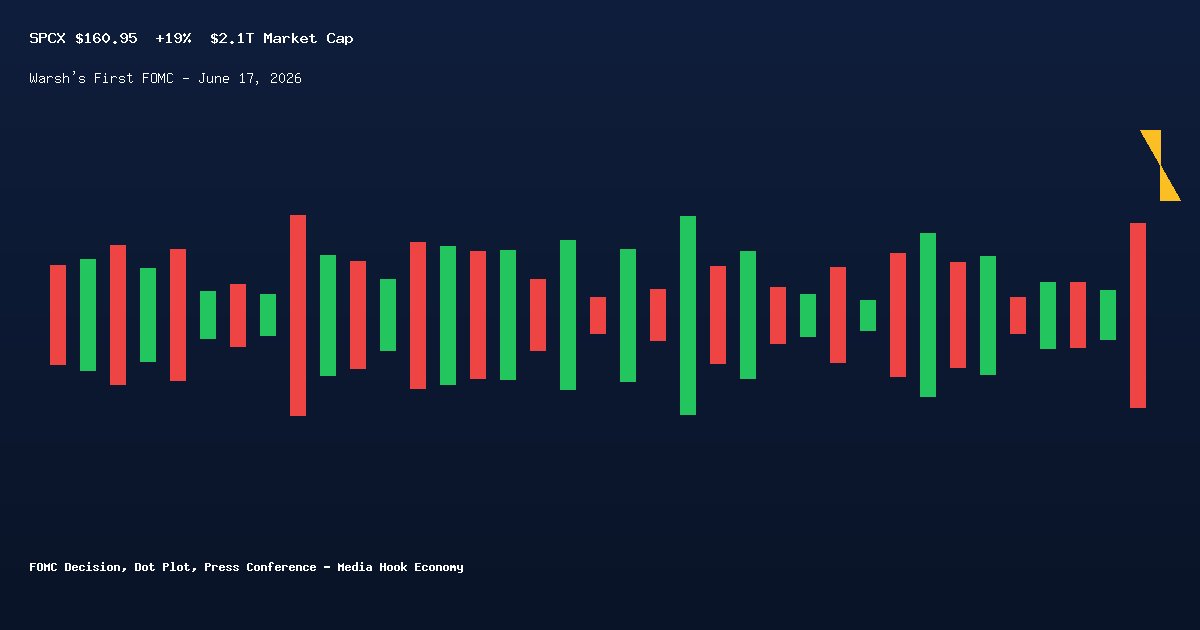

SpaceX closed at 160.95 dollars on Tuesday, June 16, 2026, putting the company’s market capitalization above 2.1 trillion dollars and overtaking Amazon, according to Investopedia and Zacks.com. The SPCX listing is the largest IPO in history by market cap, and the 19 percent single-day gain added roughly 26 billion dollars of equity value. It reprices the cost of capital for the private-credit and late-stage venture complex, and it does so two days before Kevin Warsh chairs his first Federal Reserve rate-setting meeting.

Market Reaction: Equities Ripped, the Long End Did Not Care

The Dow Jones Industrial Average closed at a record high on Tuesday, led by chip names Apple, Micron, Nvidia, Broadcom, and SanDisk, the five most-viewed tickers on Zacks.com this week. The chip complex added another leg as hyperscaler orders for HBM3E and HBM4 memory continued to outrun supply. SpaceX was the headline, but the move in the memory complex is the second-derivative story, because it tells the market that the AI capex regime has shifted from “is the order book real” to “can supply keep up.” The Treasury market did not join the party. The 30-year auction on June 11 cleared at 4.84 percent, the weakest tail of the year, and the long end has stayed heavy ever since. The 2s10s curve sat at 22 basis points at the close, the flattest since March 2023, a tell that the bond market is not buying the equity-market signal. The OIS-implied probability of a September cut dropped to 38 percent from 56 percent a month ago.

The Numbers: Three Hard Data Points and a Quote That Frames Wednesday

Three numbers frame the decision. The April nonfarm payrolls print came in at 138,000, a third consecutive miss against the consensus of 180,000, with the unemployment rate ticking up to 4.3 percent and average hourly earnings decelerating to 3.6 percent year over year, the slowest pace since June 2021. The May Consumer Price Index print came in at 4.2 percent headline and 2.9 percent core, with supercore services inflation at 3.2 percent. The April FOMC vote is the third number. Governor Stephen Miran dissented in favor of a 25 basis-point cut, and regional presidents Beth Hammack, Neel Kashkari, and Lorie Logan voted to hold but reportedly objected to language that left the door open to easing. The CME FedWatch tool put the probability of a hold at 96.8 percent going into Tuesday, with the 2026 median dot in the March SEP at 3.13 percent, implying two 25 basis-point cuts. The quote that frames Wednesday’s press conference belongs to ECM Source analyst Bruno, who summarized the April statement language this way: “the dot plot is going to spread out, not converge,” a four-word read on why the bond market is pricing the long end for a longer, higher terminal rate than the equity market is pricing the next twelve months.

What’s Driving It: The SpaceX Listing Reset the Risk Premium, the FOMC Sets the Cost of Capital

The SpaceX listing is the kind of event that resets the implicit risk premium the equity market uses to discount cash flows. A 2.1 trillion dollar market cap for a company that did not exist in the public market six months ago, on a 19 percent single-day move with no earnings cycle and no fresh guidance, is not a single-stock story. It is a signal that late-stage private capital is being repriced in real time, and that the public market is the only place large allocators can find liquidity. The venture ecosystem that priced SPCX’s last private round in early 2025 at roughly 350 billion dollars is now sitting on an asset the public market values at six times that. That delta re-marks every other late-stage private credit position, which means the next time the Fed looks at financial conditions, the SPCX print will be in the index as a tightening, not a loosening. Warsh’s first FOMC is not a meeting about whether to cut. It is a meeting about whether the cost of capital, set by the dot plot and the balance-sheet runoff, can stay restrictive enough to lean against the equity market’s new appetite for risk.

What to Watch on Wednesday: Three Catalysts That Will Move the Long End

Three things to watch on Wednesday. First, the 2026 dot plot median. A slip from 3.13 percent to 3.25 or 3.38 percent would confirm the bond market’s read on a longer, higher rate path, while a hold at 3.13 percent would be read as dovish and would likely drive the long end sharply lower. Second, the dispersion of the dots. A wide spread, with several officials wanting cuts and others holding steady, would confirm the April-meeting fractures and weaken the signal value of the median itself. Third, Warsh’s press conference at 2:30 p.m. Eastern, the first of his tenure, where he will be asked about the SpaceX listing, the May jobs and inflation prints, and the long end’s refusal to follow the equity market higher. The market is not pricing a cut on Wednesday. It is pricing the language that will follow, and the language that follows will be the language of a Chair who has to reconcile a 2.1 trillion dollar private credit repricing, a 4.84 percent long-end auction tail, and a 4.3 percent unemployment rate, all in a single dot plot. The most important number on the page Wednesday is not the rate. It is the median dot, and the spread around it.