Fed Holds Rates at 3.50%-3.75% in Chair Warsh’s First Decision as Trade War Complicates Inflation Fight

Federal Reserve Holds Rates at 3.50%-3.75% in Chair Warsh’s First Policy Decision

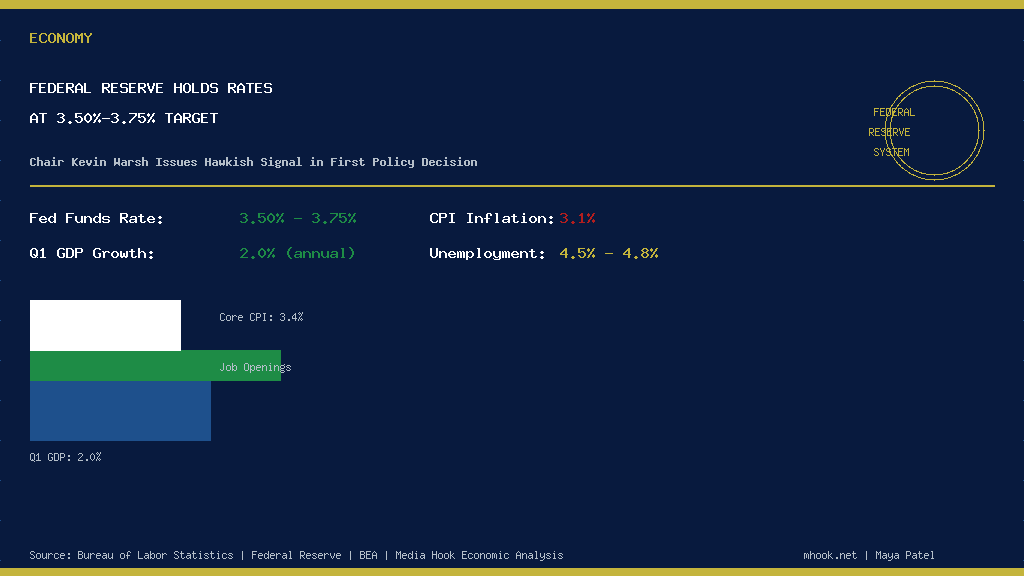

The Federal Reserve held interest rates steady at 3.50%-3.75% on Wednesday, delivering its first monetary policy decision under newly installed Chair Kevin Warsh with a unanimous 12-0 vote that surprised no one on Wall Street but sent a decidedly hawkish signal about the central bank’s resolve to keep borrowing costs elevated until inflation is decisively tamed. The Federal Open Market Committee said the unanimous decision was consistent with its dual mandate of supporting maximum employment while ensuring stable prices, and it left the door open to future rate increases if price pressures fail to subside. The decision aligned with near-unanimous market expectations, with fed funds futures pricing in better than 90% odds of no change heading into the two-day meeting, according to CME FedWatch Tool data.

Chair Warsh, who ascended to the Fed’s top post earlier this year following the departure of his predecessor, used his post-meeting statement to strike a notably cautious tone on inflation, which has proven far stickier than the central bank anticipated when it began its easing cycle. “Inflation remains elevated, and we are committed to returning it to our 2 percent objective,” Warsh said in prepared remarks released alongside the policy statement. The language marked a subtle but measurable shift from the committee’s previous communications, which had emphasized that the risks to employment and inflation were roughly in balance. That rephrasing pushed Treasury yields higher, with the benchmark 10-year note climbing to 4.68% and the two-year note — most sensitive to near-term Fed expectations — jumping to 5.12%, levels that reflect significant repricing of the rate-cut timeline over the past month.

Trade War Complicates the Inflation Outlook as Tariff Effects Ripple Through the Economy

Behind the Fed’s hawkish posture lies a maze of economic data that gives policymakers little room for complacency. The broad tariff increases that took effect in April 2026 have begun reshaping trade flows and injecting fresh upward pressure into import prices, complicating an inflation picture that was already difficult to forecast. Import figures surged at a 38% annualized rate in the first quarter as businesses front-loaded purchases ahead of the tariff implementation dates, a spike that created artificial volatility in headline GDP statistics and masked the underlying strength of domestic demand. The bounce-back in Q2 has been equally dramatic in reverse, with import volumes contracting sharply as the front-loading effect unwound, leaving economists and Fed officials alike struggling to separate signal from noise in the data stream.

Consumer price inflation, as measured by the Bureau of Labor Statistics, is running at approximately 3.1% on the headline CPI index, with the core measure — which strips out volatile food and energy components — hovering around 3.4%, still well above the Fed’s 2% target. The June 2026 CPI reading showed modest month-over-month declines in energy prices driven by easing tensions in Middle East supply corridors, offering one of the few bright spots in an otherwise challenging inflation picture. “The data are sending conflicting signals,” said one former Fed governor who requested anonymity to speak freely about ongoing deliberations. “You’ve got tariffs pushing prices up, you’ve got a cooling labor market easing wage pressures, and you’ve got an administration that is very publicly pressuring the Fed not to choke growth. It’s a genuinely difficult environment.”

GDP Growth Holds Steady But Labor Market Shows Signs of Decisive Cooling

Real GDP growth came in at approximately 2.0% at an annual rate in the first quarter of 2026, according to the BEA’s advance estimate, with the Atlanta Fed’s GDPNow model tracking a similarly modest pace for Q2 as the import contraction and tariff drag weighed on headline activity. The Philadelphia Fed’s latest Survey of Professional Forecasters painted a picture of moderate growth extending through the rest of the year, with consensus estimates clustering around 2.0% to 2.4% for full-year 2026, a pace that would represent a solid performance given the headwinds from fiscal consolidation and tighter financial conditions. Consumer spending, the backbone of the US economy, has remained resilient, with retail sales data showing households continuing to open their wallets even as elevated prices squeeze purchasing power.

The unemployment rate has risen to a range of 4.5% to 4.8%, a level that nonetheless remains low by historical standards but marks a decisive shift from the extraordinarily tight labor market of 2024 and 2025. Job openings have declined notably, and the quits rate — a closely watched indicator of worker confidence — has fallen to levels not seen since before the pandemic boom. This cooling in labor market momentum is exactly the kind of demand-side moderation the Fed has been seeking, but the inflation data suggest that price pressures are not yet responding to that cooling as quickly as the committee would like. “The Fed is in a genuine bind,” said a senior economist at a major New York bank. “Cut too early and inflation re-accelerates. Keep rates too high for too long and you break the labor market. Warsh is trying to thread that needle and he doesn’t have a lot of margin for error.”

Market Repricing Accelerates as Traders Abandon Rate-Cut Bets for 2026

Financial markets absorbed the Fed’s decision and Warsh’s hawkish commentary with a significant repricing of rate-cut expectations that had been building for months. Before Wednesday’s meeting, fed funds futures contracts had been pricing in two quarter-point rate cuts by year-end, reflecting optimism that inflation’s retreat would give the Fed room to ease. That expectation collapsed in the hours following the statement, with markets now pricing in just one cut at best and a meaningful probability of a rate increase if the next two CPI reports come in hotter than expected. The equity market initially sold off on the news before recovering most of its losses, with the S&P 500 ending the session down just 0.3%, suggesting that investors are confident the economy can absorb higher rates for a while longer without falling into recession.

The dollar strengthened against most major currencies, with the DXY index climbing to its highest level in several months as the yield differential between US Treasuries and foreign bonds widened in favor of American assets. Credit markets showed some stress at the long end, with investment-grade corporate spreads widening modestly, though the overall tone remained orderly by historical comparison. The two-year/10-year Treasury curve, which had been inverted for much of the past two years, moved to its least inverted posture since 2023, a technical shift that bond traders watch closely as a potential early signal of turning points in the economic cycle. The Fed’s next scheduled policy meeting is in six weeks, giving officials a full round of additional data — including two more CPI reports and another monthly jobs report — before they must decide whether the current stance of monetary policy remains appropriate for an economy that is growing, cooling, and still too inflationary all at the same time.

What Comes Next for the Fed as It Navigates the Narrow Path Between Inflation and Recession

The path ahead for the Federal Reserve is unusually uncertain even by the standards of a central bank that routinely deals in forecasting uncertainty. The tariff regime introduced in April 2026 is still working its way through the pricing pipeline, with many economists estimating that the full inflationary impact of the import levies has not yet shown up in consumer prices, a lag that could keep inflation elevated well into 2027 even if demand cools further. The Fed’s own Summary of Economic Projections, last updated in March 2026, showed committee members penciling in two rate cuts for the year, but those projections were produced before the tariff announcements and the subsequent hawkish shift in Warsh’s public commentary, making them largely obsolete as a forward guide.

For ordinary Americans, the practical consequences of the Fed’s decision play out in mortgage rates, credit card charges, and the cost of servicing existing debt. The 30-year fixed mortgage rate, which had dipped below 6% earlier in the year on rate-cut optimism, has climbed back above 6.75% following the recent yield spike, adding hundreds of dollars to monthly payments for prospective homebuyers and weighing on housing affordability at a time when residential investment is already contributing negatively to GDP. Small businesses, which rely heavily on short-term credit lines, face similar pressures as their borrowing costs remain elevated. Whether the Fed’s higher-for-longer stance succeeds in grinding inflation back to 2% without triggering a recession will define the economic legacy of Warsh’s early tenure — and the verdict, most analysts agree, will not arrive for at least another year of data.