Fed Holds Rates as PCE Inflation Remains Above Target and Growth Signs Waver

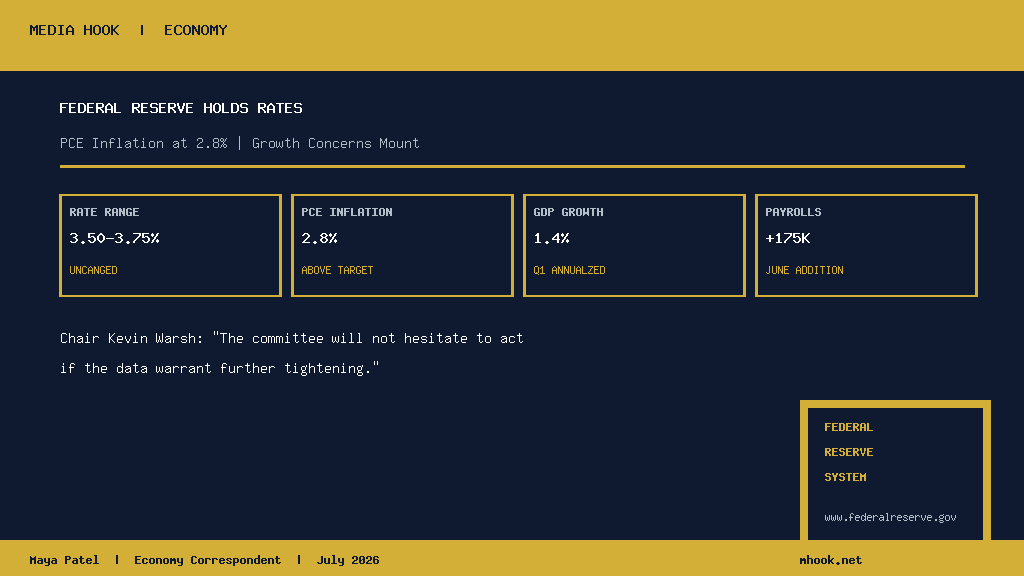

The Federal Reserve held interest rates steady at 3.50-3.75 percent on Wednesday, marking its third consecutive pause as policymakers navigated a complex economic landscape defined by stubbornly elevated inflation and increasingly uncertain growth momentum. The decision, made at the conclusion of the Federal Open Market Committee two-day meeting, arrived amid fresh data showing the Personal Consumption Expenditures price index holding at 2.8 percent year-over-year in May, still meaningfully above the central bank\’s 2 percent target. Chair Kevin Warsh struck a cautious tone in his post-meeting remarks, signaling that policymakers remain prepared to tighten further should price pressures prove persistent. \”The committee will not hesitate to act if the data warrant further tightening,\” Warsh told reporters, adding that the current stance of monetary policy remains \”appropriate but not permanently so.\”

Financial markets, which had been pricing in roughly a 65 percent probability of a rate cut by year-end before the meeting, rapidly adjusted following Warsh\’s comments, with fed funds futures now implying just a 38 percent chance of any reduction before December. The S&P 500 fell 0.9 percent in afternoon trading, while the two-year Treasury yield climbed eight basis points to 4.62 percent. The repricing underscored how thoroughly investors had misinterpreted the Fed\’s intent heading into the summer meeting season. \”We are not on a preset path,\” Warsh said. \”Every meeting is live.\”

Inflation Data Confounds the Disinflation Narrative

The May PCE report, released by the Bureau of Economic Analysis last Friday, served as the final major data point before this week\’s FOMC gathering. Headline PCE rose 0.4 percent on a monthly basis and 2.8 percent year-over-year, while core PCE, which strips out volatile food and energy components, came in at 3.2 percent annually — its highest reading since February. The persistence of services inflation, particularly in shelter and healthcare, continued to account for the bulk of the excess above target. Goods prices, which had been a deflationary force through much of 2025, have begun stabilizing, removing what had been a significant tailwind for disinflation progress. Economists at Goldman Sachs noted that the inflation picture has grown \”structurally more challenging\” since the start of the second quarter. \”The last-mile problem in disinflation has proven more difficult than anticipated,\” the Goldman team wrote in a Tuesday research note. \”We now see the risk of rates remaining at current levels through at least the first quarter of 2027.\”

Growth Indicators Send Contradictory Signals

Against the inflation backdrop, broader economic growth metrics have delivered a decidedly mixed picture. Gross domestic product growth for the first quarter came in at an annualized rate of 1.4 percent, down sharply from the 2.8 percent logged in the fourth quarter of last year. Consumer spending, which accounts for roughly two-thirds of U.S. economic activity, grew at just a 1.5 percent annualized rate in Q1, its slowest pace in two years. Retail sales for May were essentially flat compared with the prior month, suggesting that household demand is cooling as higher borrowing costs and persistent price inflation erode purchasing power. The labor market, however, has remained resilient by most measures, with the economy adding 175,000 nonfarm payroll jobs in June, beating the consensus forecast of 155,000. The unemployment rate held steady at 4.3 percent, still near multi-decade lows, though it has ticked up from the 3.7 percent floor reached in early 2025.

Markets Reprice and the Higher-for-Longer Era Extends

The repricing in financial markets following Wednesday\’s decision has been swift and consequential. The yield on the benchmark 10-year Treasury note rose to 4.51 percent from 4.39 percent before the meeting, its highest level since November. The dollar index gained 0.6 percent, extending a recent trend driven by the interest rate differential between the United States and other major economies. In the mortgage market, the 30-year fixed rate climbed to 7.18 percent, the highest since October, dealing another blow to an already-fragile housing market where existing home sales have fallen to their lowest seasonally adjusted annual pace in over a decade. Looking ahead, the trajectory of Fed policy will hinge critically on the next round of inflation data, particularly the July consumer price index report due out in August and the next PCE reading. Fed funds futures markets now price a mere 22 percent chance of any rate cut at the September meeting, down from 41 percent a week ago.